What Happens With Your Mortgage On Break Up?

Table of Contents

- Understanding Your Options

- 1. Selling the Property

- 2. Buying Out Your Partner

- 3. Your Partner Buys You Out

- 4. Keeping the Existing Arrangement

- Key Considerations

- Communication with Your Lender

- Legal Advice

- Financial Implications

- Emotional Wellbeing

- Steps to Take

- The Importance of Professional Advice

- Looking to the Future

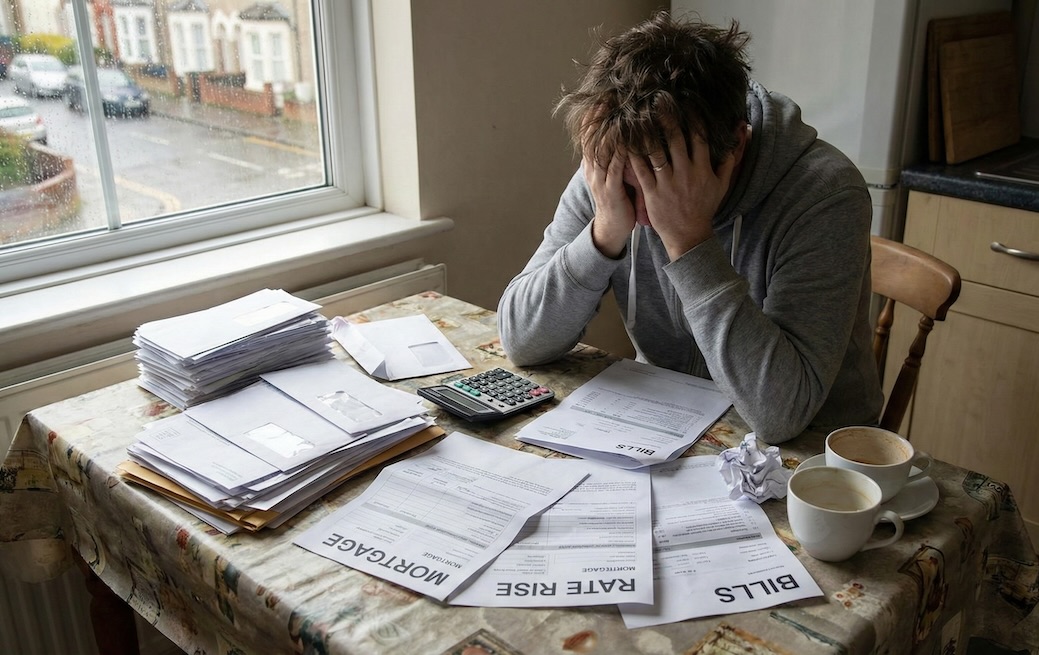

Breaking up is hard to do, as the old song goes. But when you're separating from a partner with whom you share a mortgage, it can feel like you're navigating a financial and emotional minefield. If you find yourself in this situation, you're not alone. Many couples face this challenge, and while it's undoubtedly stressful, there are ways to manage it effectively.

Understanding Your Options

When you split from your partner and have a joint mortgage, you generally have four main options:

- Sell the property and split the proceeds

- Buy out your partner's share of the equity

- Have your partner buy out your share

- Keep the property and the existing mortgage arrangement

Each of these options comes with its own set of challenges and considerations. Let's dive deeper into each one.

1. Selling the Property

This is often the cleanest break, financially speaking. You sell the house, pay off the mortgage, and split any remaining equity. However, it's not always the easiest emotionally, especially if children are involved. If you're considering this option, here are some key points to remember:

- Both parties need to agree to sell

- You'll need to agree on a selling price

- Consider the current market conditions - is it a good time to sell?

- Be prepared for potential capital gains tax if the property has increased in value

2. Buying Out Your Partner

If you want to keep the property, you might consider buying out your partner's share. This involves:

- Getting a professional valuation of the property

- Calculating your partner's share of the equity

- Securing a new mortgage in your sole name

- Proving to the lender that you can afford the mortgage payments on your own

Remember, this option requires you to qualify for a mortgage on your own income, which can be challenging.

3. Your Partner Buys You Out

This is essentially the reverse of option 2. Your partner would need to go through the same process of valuation, equity calculation, and securing a new mortgage. If you're the one moving out, this could provide you with a lump sum to start afresh.

4. Keeping the Existing Arrangement

Sometimes, especially when children are involved, couples choose to keep the existing mortgage arrangement. This might mean:

- One partner continues living in the property while the other moves out

- Both partners continue to pay the mortgage

- The property remains in both names

While this can work in the short term, it's often not a sustainable long-term solution. It can complicate future financial decisions and relationships.

Key Considerations

Regardless of which option you choose, there are several important factors to consider:

Communication with Your Lender

It's crucial to keep your mortgage lender informed about your situation. Many people worry that telling their lender about a separation could trigger negative consequences, but this is rarely the case. In fact, being open and honest with your lender can often lead to more support and flexibility.

Lenders have processes in place to deal with these situations and may be able to offer solutions such as:

- Payment holidays

- Extending the mortgage term to reduce monthly payments

- Switching to an interest-only mortgage temporarily

Legal Advice

It's highly recommended to seek legal advice when dealing with a mortgage split. A solicitor can help you understand your rights and obligations, especially if you're not married. They can also assist with:

- Drafting a formal separation agreement

- Advising on the transfer of property ownership

- Helping to negotiate a fair settlement

Financial Implications

Splitting a mortgage can have significant financial implications. Consider:

- Early repayment charges if you're ending your mortgage early

- Potential changes to your credit score

- The impact on your ability to secure future mortgages

- Tax implications, especially if you're selling the property

Emotional Wellbeing

While it's important to focus on the practical aspects, don't underestimate the emotional toll of this process. Consider seeking support from friends, family, or a professional counselor. Remember, it's okay to take time to process your emotions alongside dealing with the financial aspects.

Steps to Take

If you find yourself in this situation, here are some steps you can take:

- Communicate with your ex-partner: Try to agree on a way forward that works for both of you.

- Inform your lender: Be honest about your situation and explore what options they can offer.

- Seek legal advice: Understand your rights and obligations.

- Get a property valuation: This is crucial if one partner is buying out the other.

- Review your finances: Understand what you can afford moving forward.

- Consider your long-term goals: What do you want your living situation to look like in the future?

- Explore remortgaging options: If you're keeping the property, you may need to remortgage in your sole name.

- Update your will: Ensure your wishes are reflected in your current circumstances.

The Importance of Professional Advice

Navigating a mortgage split can be complex, and it's not something you should tackle alone. Professional advice can be invaluable in this situation. Consider speaking with:

- A mortgage advisor who can help you understand your options and potentially find new mortgage deals

- A solicitor to guide you through the legal aspects

- A financial advisor to help you plan for your future financial stability

These professionals can provide expert guidance tailored to your specific situation, helping you make informed decisions during this challenging time.

Looking to the Future

While dealing with a mortgage split can be stressful, it's important to remember that it's a temporary situation. With careful planning and the right support, you can navigate this challenge and move towards a more stable financial future.

Remember, every situation is unique, and what works for one couple may not work for another. Take the time to consider all your options, seek professional advice, and make decisions that are right for you and your family in the long term.

If you're facing a mortgage split and need expert advice, don't hesitate to reach out to a professional mortgage advisor. They can provide personalized guidance to help you navigate this challenging situation and find the best path forward for your unique circumstances.

![What Is The Minimum Down Payment (Deposit) For A House In The Uk? [2026][Short Version]](https://mortgagemapper.com/featured-images/what-is-the-minimum-down-payment-deposit-for-a-house-in-the-uk-2026-short-version.jpg)