Fixed Rate Vs Variable Rate Mortgage In The Uk (And How To Choose Without Panicking)

Table of Contents

- The Very Basics: What Are We Even Talking About?

- The Fixed Rate Mortgage: The "Comfort Blanket"

- Why People Love Fixed Rates (The Pros)

- The Downside of the Comfort Blanket (The Cons)

- The Variable Rate Mortgage: Riding the Rollercoaster

- 1. The Tracker Mortgage

- 2. The Standard Variable Rate (SVR)

- Why People Choose Variable Rates (The Pros)

- The Fear Factor (The Cons)

- The Great Debate: Fixed Rate vs Variable Rate Mortgage in the UK Today

- Making the Decision: It's About You, Not Just the Maths

- Don't Do It Alone

Buying a house in the UK right now feels a bit difficult, it’s exciting and It’s the dream, but it’s also incredibly stressful.

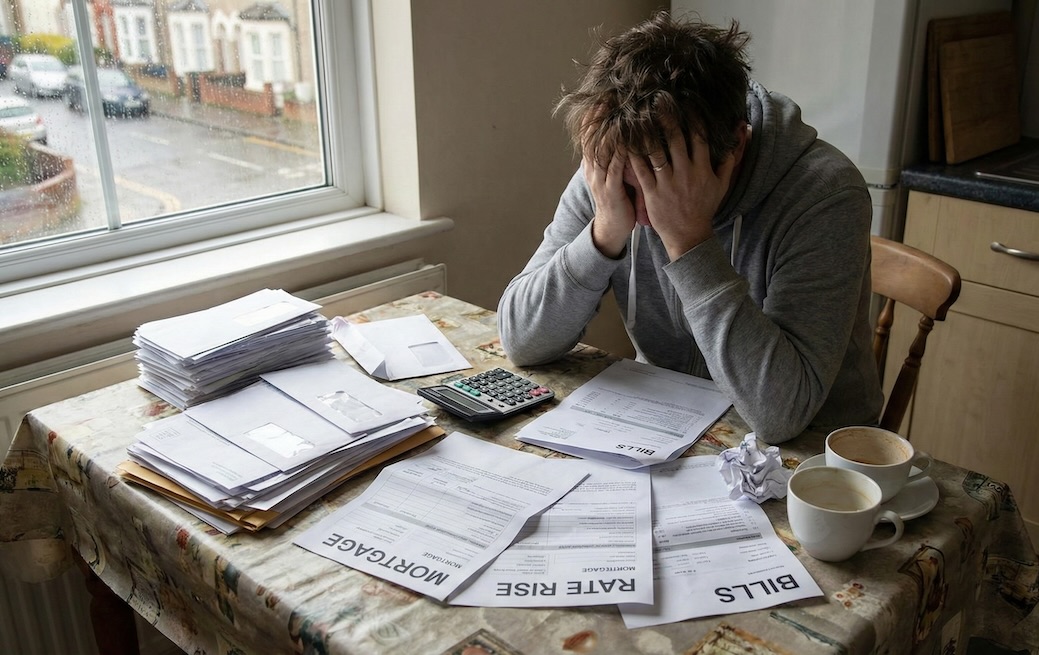

If you’ve been reading the news headlines about interest rates, inflation, and house prices, you might feel a tight knot in your stomach. This isn't just about numbers on a spreadsheet, this is about your home, your sanctuary, and your future financial safety.

When you finally get to the stage of actually picking a mortgage, you are faced with the most important of all financial decisions. The one that keeps prospective buyers awake at 3 am staring at the ceiling.

The choice between a Fixed Rate vs variable Rate Mortgage in the UK.

It sounds complicated. It sounds dull. But getting this decision right is crucial for your peace of mind (and your wallet).

At Mortgage Mapper, we believe in plain English and helping you feel confident. So, grab a cup of tea, take a deep breath, and let’s break this down simply and clearly so you can take the right decision for you.

The Very Basics: What Are We Even Talking About?

Before we dive into the battle of fixed vs. variable, let's strip it right back.

When you get a mortgage, a lender (like a bank) lends you a huge chunk of money to buy a property. They don’t do this out of the goodness of their hearts. They charge you for the privilege.

That charge is called interest.

Every month, you pay back a bit of the original loan amount (the capital), plus the interest charge for that month.

The big question is: How is that interest charge calculated?

Does it stay the same forever? Or does it change based on what the economy is doing? That is the entire difference between fixed and variable rates.

The Fixed Rate Mortgage: The "Comfort Blanket"

Imagine you sign up for a new mobile phone contract. You agree to pay £30 a month for two years. It doesn't matter if the phone company’s costs go up, or if inflation goes wild. You pay £30. That’s it. You know exactly where you stand.

A fixed-rate mortgage works exactly like that.

You agree with the lender on a specific interest rate—say, 4.5%—for a set period. The most common periods in the UK are 2 years or 5 years, though you can sometimes find 10-year fixes.

Why People Love Fixed Rates (The Pros)

The biggest benefit here is emotional: Certainty.

In a world where the price of your weekly food shop seems to go up every time you blink, knowing exactly what your biggest monthly bill will be is incredibly soothing. It allows you to budget. You can plan holidays, nursery fees, or saving for a car, safe in the knowledge that your mortgage payment won’t suddenly jump up by £200 next month because some bankers in London decided to raise rates.

It’s financial peace of mind. It’s a safety net.

If you want to see what those reliable monthly payments might look like for you, have a quick play with our Monthly Repayments Calculator. It helps turn these abstract percentages into real pounds and pence.

The Downside of the Comfort Blanket (The Cons)

Nothing in life is free, and that certainty comes at a price.

- The "Just In Case" Premium: Lenders aren't stupid. If they guarantee your rate for five years, they are taking a risk that rates might rise. To cover that risk, fixed rates are often slightly higher at the start than the best variable rates available at the same time. You are paying a little extra for the insurance of knowing your payment won't change.

- FOMO (Fear Of Missing Out): This is the psychological kicker. Imagine you fix your mortgage today at 5% for five years. Next year, the economy settles down and interest rates plummet to 3%. Everyone else is celebrating their cheaper mortgages, but you are stuck paying 5% for another four years. It can be incredibly frustrating.

- Locked In: If your circumstances change drastically and you need to exit that mortgage early (perhaps to move house unexpectedly), you will usually face stiff penalties called Early Repayment Charges (ERCs). The comfort blanket is tied on very tightly.

The Variable Rate Mortgage: Riding the Rollercoaster

If a fixed rate is a steady train ride, a variable rate is a rollercoaster. It might be thrilling, and it might be faster, but there are going to be ups and downs that might make you scream.

With a variable rate mortgage, the interest rate you pay can change.

If it changes, your monthly payments change. Sometimes they go down (yay!), and sometimes they go up (ouch!).

There are two main types of variable rates you need to know about in the UK:

1. The Tracker Mortgage

This does exactly what it says on the tin: it "tracks" something else. Almost always, it tracks the Bank of England Base Rate.

If the Bank of England puts interest rates up by 0.25% to combat inflation, your mortgage rate goes up by exactly 0.25% the next month. If they cut rates, your mortgage gets cheaper. It’s transparent. You know exactly why your payments are changing.

2. The Standard Variable Rate (SVR)

This is the lender's "default" rate. If your fixed deal ends and you don't do anything, you get dumped onto this.

Warning: SVRs are almost always expensive. The lender can change this rate pretty much whenever they like. They don't have to follow the Bank of England. You generally want to avoid sitting on an SVR if you can help it.

Why People Choose Variable Rates (The Pros)

Why would anyone choose uncertainty? Usually, because it’s cheaper right now.

Variable rates often start lower than fixed rates because you aren't paying that "insurance premium" for certainty. You are taking on the risk yourself.

Furthermore, tracker mortgages are often more flexible. They might have smaller (or no) Early Repayment Charges, meaning if you plan to move house soon or want to overpay massively on your mortgage, a tracker might be easier to get out of.

The Fear Factor (The Cons)

The downside is obvious: Uncertainty.

If you are stretched to your financial limit just paying the mortgage today, a variable rate is terrifying. If rates rise significantly over the next two years, could you afford an extra £100, £300, or £500 a month?

If the thought of your mortgage payment going up makes you feel physically sick, a variable rate probably isn't for you.

The Great Debate: Fixed Rate vs Variable Rate Mortgage in the UK Today

So, why is this decision so incredibly difficult right now?

If we were in a period where nothing much was changing in the economy, it would be an easier choice. But we are living through interesting economic times in the UK. We've seen rates shoot up rapidly after years of being historically low.

The debate around Fixed Rate vs variable Rate Mortgage in the UK currently boils down to this:

Do you believe interest rates have peaked and are about to fall? Or do you fear they might stay high or climb even further?

- The Gambler's View: "Interest rates are surely going to drop soon. I'll take a cheaper 2-year tracker now. Yes, it might go up a tiny bit in the short term, but in a year's time, rates will crash, and I'll be paying much less than the people who fixed."

- The Cautious View: "The world is unstable. Inflation is sticky. I can just about afford the payments now. I cannot take the risk of them going up further. I'm locking in a 5-year fix. Even if rates drop later, at least I know I can keep the roof over my head."

It's hard to know who to believe. To get a sense of the wider context of the UK property market, it's always worth looking at the bigger picture. Our UK Housing Data Hub can give you some background on what's happening across the country.

Making the Decision: It's About You, Not Just the Maths

Ultimately, this isn't just a maths problem. It's a psychology problem.

There is no single "correct" answer to the Fixed Rate vs variable Rate Mortgage in the UK debate. What was right for your parents ten years ago, or your best mate last week, might be totally wrong for you today.

You need to ask yourself some honest questions:

- How tight is your budget? If you have zero wiggle room at the end of the month, gambling on a variable rate is incredibly risky.

- How well do you sleep? Seriously. If not knowing your future outgoings is going to cause you anxiety, pay the extra for the fixed rate. Peace of mind has a value.

- What are your future plans? Are you staying in this house for five years, or might you move in two? This affects how locked-in you want to be.

Don't Do It Alone

This is the biggest debt you will likely ever take on. It involves hundreds of thousands of pounds. Yet, so many people try to guess the answer based on something they read in a Sunday newspaper.

The stakes are too high to guess.

The best way to navigate the choice between fixed and variable rates is to talk to a human being who lives and breathes this stuff every day. A qualified mortgage adviser doesn't just look at the rates; they look at you. They look at your finances, your attitude to risk, and your future plans, and they recommend what is best for your unique life.

At Mortgage Mapper, we make that easy. You fill in one simple form, and we match you with the right expert for your situation.

Don't lose sleep worrying if you made the right choice. Get expert advice and move forward with confidence.

![What Is The Minimum Down Payment (Deposit) For A House In The Uk? [2026][Short Version]](https://mortgagemapper.com/featured-images/what-is-the-minimum-down-payment-deposit-for-a-house-in-the-uk-2026-short-version.jpg)

![What Is The Minimum Down Payment (Deposit) For A House In The Uk? [2026][Long Version]](https://mortgagemapper.com/featured-images/the-definitive-guide-to-the-minimum-down-payment-for-a-house-navigating-the-2025-uk-property-market.png)