The 2026 Mortgage Cliff: How To Protect Your Home And Your Wallet

Table of Contents

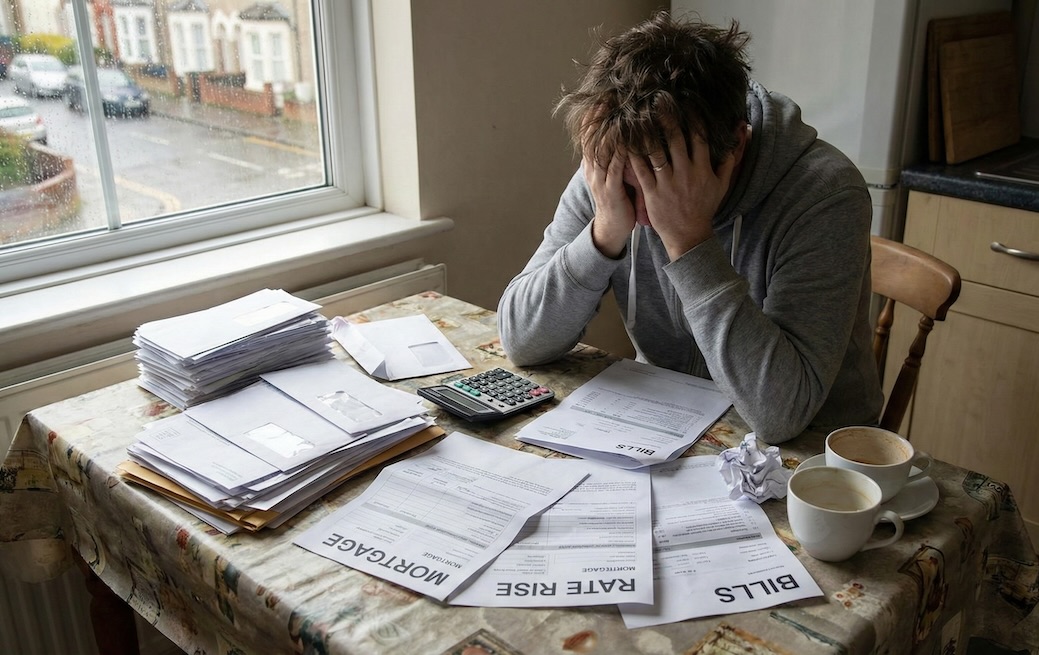

If you bought your home or remortgaged back in 2021, you probably remember feeling like you’d won the lottery. Interest rates were incredibly low, sometimes under 2%. It felt like "cheap money," and many of us signed up for five-year fixed deals, thinking we’d tucked ourselves away safely from the chaos of the world.

Well, it is now 2026, and for nearly one million UK households, that safety bubble is about to pop.

Why are costs jumping now?

Back in 2021, the Bank of England base rate was a tiny 0.1%. Today, even after some recent welcome drops, it sits at 3.75%. If you’ve been "shielded" by a five-year fix, you haven’t felt the sting of the market turmoil that started a few years ago.

But as those deals end this year, reality is biting. On average, families moving off these old rates are looking at an extra £2,124 a year in repayments. That is about £177 more every single month. That’s a lot of grocery trips or family days out. To see exactly how your own numbers might change, you can use our Monthly Repayments Calculator to get a clear picture.

The "Hidden" Trap: Don’t Just Do Nothing

When your fixed deal ends, your bank will automatically move you onto their Standard Variable Rate (SVR). This is often their most expensive rate.

For example, if you stay on a typical SVR of around 7.24%, your monthly bill could jump from £755 to a staggering £1,226. That is an extra £471 a month! It’s vital to check for Hidden Costs and make a plan before your current deal expires.

Is there any good news?

Actually, yes. While rates are higher than they were in 2021, they are much better than the "scary" peaks we saw a year or two ago. The market has stabilised, and there are still great deals out there, you just have to find them.

If you’re worried about what you can actually afford in today's market, our Affordability Calculator can help you set a realistic budget. You can also keep an eye on Average House Prices to see how your home’s value has changed, which might help you get a better "Loan to Value" deal.

Take Control of Your Future

It's okay to feel a bit stressed. Your home is your sanctuary, and seeing the costs go up is scary. But the worst thing you can do is wait until the last minute.

The best way to lower the "interest rate sting" is to shop around. You don't have to do this alone. At Mortgage Mapper, we believe everyone deserves an expert in their corner. We can match you with a professional who knows the 2026 market inside and out.

Don't wait for the bank to send you a scary letter. Take the first step today and Find a Mortgage Adviser who can help you navigate the 2026 cliff and keep your monthly payments as low as possible.

Would you like me to help you calculate your potential savings by comparing a few different interest rate scenarios?

![What Is The Minimum Down Payment (Deposit) For A House In The Uk? [2026][Short Version]](https://mortgagemapper.com/featured-images/what-is-the-minimum-down-payment-deposit-for-a-house-in-the-uk-2026-short-version.jpg)

![What Is The Minimum Down Payment (Deposit) For A House In The Uk? [2026][Long Version]](https://mortgagemapper.com/featured-images/the-definitive-guide-to-the-minimum-down-payment-for-a-house-navigating-the-2025-uk-property-market.png)