What Documents Do You Need For A Mortgage: A Complete Listicle

Table of Contents

- TL;DR

- List Item 1: Proof of Identity Documents

- List Item 2: Income Verification Documents

- What a salaried employee should hand over

- Self‑employed? Here’s the deeper dive

- What about mixed income?

- Extra documents that can tip the scales

- How to keep everything tidy

- List Item 3: Credit History and Debt Documents

- What counts as a credit history document?

- How to present your debt information for maximum clarity

- Common pitfalls – and how to avoid them

- Quick checklist before you hit “submit”

- List Item 4: Property and Asset Documentation (Table Included)

- What exactly counts as “property and asset” paperwork?

- List Item 5: Additional Supporting Documents

- Gift letters for a cash contribution

- Rental income proof for buy‑to‑let or spare rooms

- Home insurance declarations

- Divorce or separation agreements

- Legal settlements or inheritance documents

- FAQ

- What documents do I need for a mortgage if I’m a first‑time buyer?

- Do I need to provide proof of my deposit source?

- How far back should my bank statements go?

- What if I’m self‑employed or have mixed income?

- Are rental income and buy‑to‑let documents required?

- Do I need a valuation or survey before applying?

- What extra paperwork can make my application stand out?

- Conclusion

Picture this: you’ve found your dream flat in Manchester, the price tag feels right, and you’re ready to make an offer. Then the lender asks, “What documents do you need for a mortgage?” and suddenly you’re scrambling for paperwork you didn’t even know existed.

First up, the basics: a valid photo ID (passport or driving licence) and a recent utility bill or council tax statement to prove where you live. It sounds simple, but I’ve seen people lose weeks because the utility bill was older than three months, so double‑check the date.

Next, your income proof. If you’re a salaried employee, gather your last three payslips and an annual P60. For self‑employed folks, it’s a bit more involved – you’ll need your last two years of SA302 tax calculations, full tax returns, and a profit‑and‑loss statement. One client of mine, a freelance graphic designer, saved a ton of stress by using an accountant to pull a clean summary ahead of time.

Bank statements are another staple. Lenders usually want the last three months of every account you hold – current, savings, and any joint accounts. Highlight any large deposits and be ready to explain them; a sudden £5,000 influx could raise eyebrows if you can’t back it up.

Don’t forget existing mortgage statements if you’re remortgaging, plus details of any other loans or credit cards. A quick spreadsheet of monthly outgoings helps the lender see your affordability at a glance.

Here’s a practical checklist you can copy‑paste into a notes app:

- Photo ID (passport/driver’s licence)

- Proof of address (utility bill, council tax)

- Last 3 payslips + P60 (or SA302 & tax returns for self‑employed)

- 3 months of bank statements for all accounts

- Current mortgage statement (if applicable)

- Details of other debts or credit commitments

Once you’ve gathered everything, scan or photograph each document and store them in a dedicated folder – naming each file clearly, like “2024‑03‑Payslip‑March.pdf”. This makes uploading to your lender’s portal a breeze.

If you’d rather have a professional walk you through the list, you can find a mortgage advisor near you who will double‑check you haven’t missed anything and even spot opportunities to improve your rate.

And a little post‑mortgage tip: after the keys are in hand, you’ll probably start thinking about how to make the space feel like home. A quick read of an area rug size guide can help you plan the perfect first‑room makeover.

Bottom line? Treat the document hunt like a mini project: set a deadline, use a checklist, and keep everything digital. By the time the lender asks for them, you’ll have everything at your fingertips, and the mortgage process will move forward without unnecessary hiccups.

TL;DR

Gathering the right paperwork, photo ID, proof of address, recent payslips or tax returns, three months of bank statements, and any existing mortgage details, lets you breeze through the lender’s checklist and keep the mortgage process moving.

With this simple checklist in hand, you’ll avoid delays, stay organized, and feel confident securing your new home.

List Item 1: Proof of Identity Documents

Okay, let's talk about the very first thing lenders will ask for: proof of who you are. It sounds almost too simple, but if you get this wrong you’ll end up chasing documents for days, and that’s the last thing you want when you’re already juggling offers and viewings.

First off, you need a valid, government‑issued photo ID. In the UK that usually means a passport or a driving licence. If you’ve got a passport that’s still good for at least six months, you’re set. A driving licence works too, just make sure the photo is clear and the expiry date is visible.

But here’s a little nuance most people overlook: if you’re a non‑UK resident applying for a mortgage, you might also need a Biometric Residence Permit (BRP) or a visa that shows your right to live here. It’s the sort of detail that trips up a lot of first‑time buyers.

Next, you’ll need a proof‑of‑address document. A recent utility bill, council tax statement, or a bank statement that shows your current address works. The key is the date – most lenders want something dated within the last three months. I’ve seen people hand over a 2019 water bill and the underwriter raises an eyebrow. Double‑check the timestamp before you scan.

So, what should you actually gather?

- Passport (or UK driving licence) – front and back, clear scan.

- If applicable, Biometric Residence Permit or visa page.

- Utility bill, council tax bill, or bank statement dated within the last 90 days.

- Any official letter from a government body that confirms your address (e.g., HMRC correspondence).

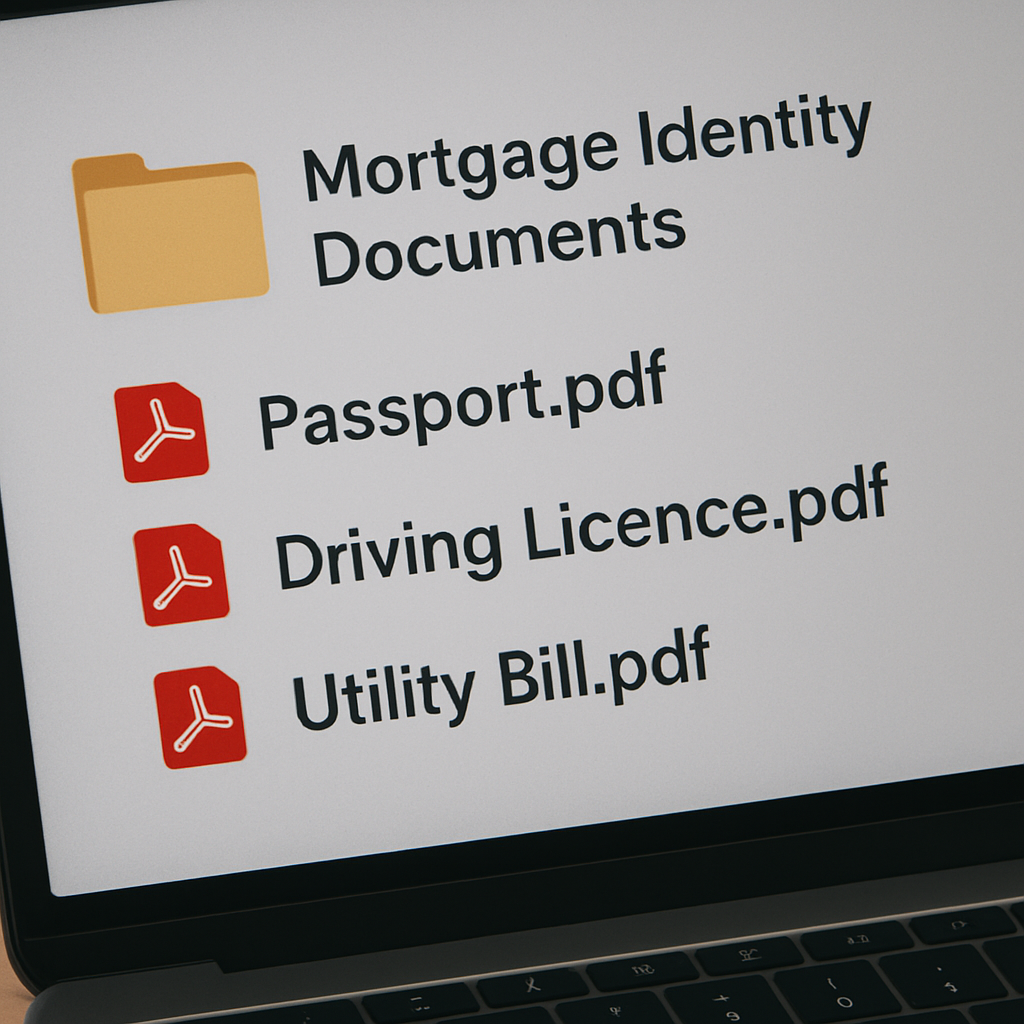

Tip: name each file consistently, like "2024-03‑Passport.pdf". It makes uploading to the lender’s portal painless and shows you’ve got your act together.

And while we’re on the topic of staying organized, think about this scenario: you’ve just finished a kitchen renovation on your rural home and you need to prove that the address you’re using is still your primary residence. A quick photo of the newly‑installed farmhouse kitchen can act as a visual cue when you upload your proof‑of‑address – it’s not required, but it adds a personal touch that can help the underwriter match your paperwork to the property.

Speaking of renovations, if you ever run into unexpected home‑maintenance issues after you’ve moved in – say a burst pipe in the kitchen – you’ll want to have a clear record of how quickly you dealt with it. It’s not a document you hand over now, but keeping a step‑by‑step guide of what you did (and any professional invoices) can be useful later if the lender asks for proof of property condition.

Here’s a quick sanity check before you hit ‘submit’:

- Is the photo ID unexpired and legible?

- Does the address proof show a date within the last 90 days?

- Are the file names consistent and easy to locate?

If you answered “yes” to all three, you’re in good shape. If not, take a few minutes now to replace any outdated documents – it’ll save you a week of back‑and‑forth later.

And just in case you’re visual‑learner, here’s a short video that walks you through scanning and naming your documents correctly.

https://www.youtube.com/embed/ER2Ajej8Rmo

After you’ve got your IDs and address proof sorted, the next step is gathering income evidence – but that’s a whole other story. For now, treat this checklist as your passport to a smoother mortgage application.

List Item 2: Income Verification Documents

List Item 2: Income Verification Documents

Alright, now that your ID is sorted, the next hurdle is proving you actually bring the money to the table. Lenders want a clear picture of what’s coming in each month, and they’ll ask for a handful of specific documents to build that picture.

What a salaried employee should hand over

First up, if you’re on a regular payroll, the magic trio is:

- Last three payslips – the most recent ones, showing your gross and net pay.

- Your most recent P60 – that end‑of‑year summary that confirms your total earnings and tax paid.

- Employment contract (optional but helpful) – it proves your role, start date, and whether you’re on a permanent or fixed‑term basis.

Why three payslips? Lenders look for consistency. A single payslip could be an outlier; three give them a short trend line. And the P60 is the accountant’s stamp that the numbers you’re showing match what HMRC has on record.

So, what if you’ve just started a new job and only have one payslip? It’s okay to explain the situation, but be prepared to provide a letter from your employer confirming your salary and start date. That little note can save you from a back‑and‑forth email chain.

Self‑employed? Here’s the deeper dive

Being your own boss means a few more pieces of paper, but the principle is the same: prove stable, sufficient income.

Typical self‑employed package includes:

- SA302 tax calculation for the last two tax years – this is the HMRC‑generated summary that shows your declared profit.

- Full tax returns (the accompanying self‑assessment pages) – they give the lender confidence you’ve reported everything.

- Profit‑and‑loss statement prepared by an accountant – a clean, professional summary of revenue versus expenses.

Many borrowers wonder, “Do I really need two years of tax docs?” The answer is usually yes, because lenders want to see that your earnings aren’t a one‑off spike. If you have a strong upward trend, highlight it in a short cover note – it can turn a potential red flag into a positive.

And a quick tip: ask your accountant to format the P&L in a simple table with clear headings. Lenders love tidy spreadsheets; it speeds up their assessment and reduces the chance of “missing information” emails.

What about mixed income?

Maybe you’re juggling a part‑time salary and a side‑hustle. In that case, blend the two approaches:

- Provide the three payslips and P60 for your salaried work.

- Supply the SA302 and tax return for the self‑employed portion.

- Include a brief summary that adds the two streams together, showing your total net monthly income.

This gives the lender a single, easy‑to‑read figure instead of a patchwork of documents.

Ever heard someone say, “I don’t have a P60 because I’m on a zero‑hour contract”? If that’s you, request a “statement of earnings” from your payroll department. It’s basically the same information, just labelled differently.

Extra documents that can tip the scales

Sometimes lenders ask for a bit more detail, especially if you have irregular income or recent bonuses.

Consider adding:

- Bonus letters or commission statements – they show additional, repeatable cash flow.

- Bank statements that trace the salary deposits – a quick visual match between payslips and actual cash coming in.

- Rental income statements if you own a buy‑to‑let property – include the tenancy agreement and recent rent receipts.

These extras aren’t always mandatory, but they can shave days off the approval timeline by pre‑empting “explain this deposit” questions.

One client of mine was stuck because a £3,000 lump‑sum from a freelance project showed up on his bank statement with no paperwork. He simply uploaded the corresponding invoice and a short note, and the lender cleared it in minutes.

How to keep everything tidy

Before you hit the lender’s portal, do a quick sanity check:

- All documents are scanned at 300 dpi or higher – blurry files get rejected.

- File names follow a simple pattern, e.g., “2024‑03‑Payslip‑March.pdf”.

- Everything is dated within the last six months – older documents look stale.

And store them in a dedicated “Mortgage‑Income” folder on your phone or cloud. When the portal asks for “income verification”, you’ll be able to drag‑and‑drop in seconds.

Bottom line: whether you’re on a payroll or running your own business, the goal is to give the lender a crystal‑clear snapshot of consistent earnings. Gather the right payslips, tax docs, and any supporting letters now, and you’ll avoid the dreaded “additional information required” emails that drag the process out.

List Item 3: Credit History and Debt Documents

Alright, we’ve covered who you are and what you earn – now the lender wants to peek at the other side of your financial story: your credit history and any existing debts.

Why does this matter? Think of it as the lender’s way of checking whether you’ve been good at paying back money in the past. A solid credit record can shave months off the approval timeline, while hidden debts can raise red flags that stall the process.

What counts as a credit history document?

Most UK lenders will ask for a recent credit report – usually the one you can pull from Experian, Equifax or TransUnion. You don’t have to pay for it; a free statutory report is enough.

Ask yourself: have you checked that report lately? If you spot an error, now’s the time to dispute it before you upload anything. A single mistaken missed payment can look like a nightmare to a mortgage underwriter.

Every loan, credit‑card balance, or finance agreement you still owe should be on the table. Lenders typically request:

- Credit‑card statements for the last three months – they show the balance, the credit limit, and your repayment pattern.

- Personal loan statements (including payday or “buy now, pay later” agreements) – the original loan agreement if you have it.

- Student loan statements – a simple summary from the Student Loans Company works.

- Car finance or hire‑purchase agreements – the latest statement that lists the outstanding amount.

- Any existing mortgage statement if you’re remortgaging – this lets the new lender see what you already owe on property.

Don’t forget joint debts if you’re applying with a partner. Even a small joint credit‑card balance shows up on the combined affordability calculation.

So, what should you actually upload?

- PDF or high‑resolution image (300 dpi or higher) of each statement.

- File names that are crystal‑clear, e.g., “2024‑04‑Barclay‑Card‑Statement.pdf”.

- Make sure the document covers the full statement period – lenders hate cropped pages.

How to present your debt information for maximum clarity

One trick that saves a lot of back‑and‑forth is to create a one‑page summary. List each debt, the creditor, the current balance, the monthly repayment, and the interest rate. This “debt snapshot” can be a simple Word table or an Excel sheet.

Here’s why it works: the underwriter can see at a glance how much of your income is already earmarked for repayments, and they can instantly run a debt‑to‑income (DTI) ratio. If the DTI looks healthy (most lenders like under 45 %), you’re much less likely to get an “additional information required” email.

And remember, honesty is the best policy. Hiding a small store‑card balance might feel harmless, but once the lender does a hard credit check, that hidden line will appear and could cause a delay.

Common pitfalls – and how to avoid them

Missing a recent credit‑card statement is a classic mistake. Lenders often ask for the most recent three months, not just the latest one. If you’ve just paid off a balance, include the statement that shows a zero balance – it proves you actually cleared the debt.

Another trap: forgetting to include “buy now, pay later” (BNPL) agreements. Even though they’re not traditional credit, many lenders treat them as debt. Grab the email confirmation or the merchant’s statement that shows the outstanding amount.

Lastly, watch out for old debts that are still showing as “active”. If a loan was settled a year ago but the record hasn’t been updated, request a clearance letter from the creditor and upload that alongside the original statement.

Quick checklist before you hit “submit”

- Credit report from Experian, Equifax or TransUnion – no older than 30 days.

- Three months of credit‑card statements for each card you hold.

- All personal loan, car finance, and student loan statements.

- Current mortgage statement (if applicable).

- One‑page debt summary with balances, repayments, and interest rates.

- High‑resolution scans, clear file names, and everything dated within the last six months.

Got all that? Great. You’ve just turned a potentially messy part of the mortgage puzzle into a tidy, transparent picture. The lender will see you as a low‑risk borrower, and you’ll move one step closer to unlocking the front door of your new home.

List Item 4: Property and Asset Documentation (Table Included)

Alright, we’ve nailed identity, income and credit – now it’s time to talk about the bricks and the bits that sit behind them. Lenders want a crystal‑clear picture of what you already own and what you’re planning to bring into the mortgage equation.

Think of it as showing the bank the puzzle pieces you already have on the table before you ask them to hand you the final piece. If you own a home already, a buy‑to‑let, or even a hefty portfolio of assets, you’ll need to pull together a handful of key papers.

What exactly counts as “property and asset” paperwork?

First off, the basics: the title deed or conveyance document for any property you already own. This proves you’re the legal owner and shows any existing charges or mortgages attached to it.

Next up, a recent valuation or market appraisal. Lenders love numbers, so a professional valuation from a RICS‑registered surveyor gives them confidence in the current market value of the asset you’re showcasing.

Got a rental property? Then you’ll need a landlord statement or tenancy agreement, plus at least six months of rent rolls to prove the cash flow is steady. For investment properties, a full schedule of income and expenses (service charges, insurance, management fees) works wonders.

And don’t forget the less obvious items – things like a recent building survey (if you’ve done a HomeReport or structural survey), a leasehold pack if the property is leasehold, and any service charge accounts if you’re buying a flat.

So, what should you actually upload? Here’s the quick cheat‑sheet we’ve all been looking for.

| DocumentWhy it mattersPro tip | ||

| Title deed / conveyance | Shows legal ownership and any existing charges | Scan at 300 dpi, keep the full page visible |

| Professional valuation | Confirms current market value for underwriting | Ask the surveyor for a digital PDF copy |

| Leasehold pack (if applicable) | Details ground rent, service charges, lease length | Highlight the remaining lease term – >80 years is ideal |

| Rental income evidence | Demonstrates cash flow from investment properties | Include rent rolls + tenancy agreements for the last 6 months |

| Building survey / HomeReport | Assures the property is structurally sound | Use the summary page – lenders rarely need the full report |

Notice how each row gives you a “why” and a tiny hack to keep the process smooth. It’s those little details that stop the dreaded “missing information” emails from popping up.

Now, let’s talk about assets beyond real estate. If you’ve got a sizable savings pot, a pension fund, or even a stock portfolio, pull the latest statements. A one‑page summary that lists the asset type, current value, and the institution holding it can be a lifesaver.

Why bother? Because lenders use your total asset pool to calculate the loan‑to‑value (LTV) ratio. The higher your net assets, the more leeway they have to offer you a better rate. A quick tip: if you have a high‑interest savings account, ask the bank for a “balance confirmation” letter – it’s a tidy, official way to prove the cash you’ve got sitting there.

What about joint assets? If you’re applying with a partner, include both of your ownership documents. Even if only one name appears on the title, the other partner’s contribution can be highlighted in a short cover note, explaining the shared equity.

And here’s a little story from a client of mine: she was applying for a first‑time buyer mortgage but also owned a small cottage she rented out on weekends. She thought the cottage was irrelevant, but once we uploaded the lease agreement and the last six months of rent receipts, the lender saw an extra £250 a month of income. That extra buffer shaved a few percentage points off her rate.

Bottom line? Gather the title deeds, valuation reports, lease packs, rental evidence, and any other asset statements, scan them cleanly, name them clearly (e.g., “2024‑04‑Cottage‑Title.pdf”), and you’ll hand the lender a tidy, persuasive portfolio that says, “I’m organized, I’m solvent, let’s do this.”

List Item 5: Additional Supporting Documents

So you’ve already got your ID, income proof, credit history, and property paperwork lined up – great start. But lenders love a little extra evidence that shows you’re low‑risk and ready to roll. That’s where the “additional supporting documents” come in.

Gift letters for a cash contribution

If a family member is helping you with a deposit, the lender will ask for a signed gift letter. It should state the amount, confirm it’s a gift (no repayment expected), and include the giver’s contact details. A quick tip: ask the donor to attach a recent bank statement that shows the money left their account – that way the lender sees the trail in one go.

Rental income proof for buy‑to‑let or spare rooms

Got a flat you let out, or you’re still receiving rent from a previous property? Upload the tenancy agreement plus the last six months of rent rolls. If you’re on a short‑term platform like Airbnb, a summary of earnings and a copy of the platform’s payout statements works just as well. Those numbers can boost your affordability calculation, especially if you’re a first‑timer.

Home insurance declarations

Many lenders request a copy of your home insurance policy or a “certificate of insurance” before they’ll finalise the loan. It proves the property is protected against fire, flood, or other risks. If you haven’t chosen a policy yet, a quote from a reputable insurer (with the premium amount shown) usually satisfies the requirement.

Divorce or separation agreements

Going through a divorce? The lender will want to see the settlement agreement that outlines how assets and liabilities are split. Upload the signed decree and any accompanying financial statements. It clears up any ambiguity about who owns what, and it stops the underwriter from guessing your true net worth.

Legal settlements or inheritance documents

Received a lump‑sum inheritance or a legal settlement? Include the probate order or settlement letter that details the amount you’ve received. Pair it with a bank statement showing the funds deposited. This extra cash can be treated as an asset, pushing your loan‑to‑value ratio in your favour.

Wondering how to keep all these extras tidy? Create a “Mortgage Extras” folder on your phone or cloud, and name each file with a date and brief description – e.g., “2024‑05‑Gift‑Letter‑Mom.pdf”. Consistent naming saves you minutes when the portal asks for “additional supporting documents”.

And here’s a little insider secret: some lenders now let you link your bank account directly for real‑time verification of assets and deposits. Fannie Mae explains that this digital process can cut down the back‑and‑forth of uploading statements, but only if you give explicit permission. If you’re comfortable, it’s a smooth way to prove the extra cash without hunting down PDFs.

Still not sure which extra docs you might need? Ask yourself: “Do I have any money that isn’t covered by my main bank statements?” “Is there any agreement that changes my ownership picture?” If the answer is yes, dig out that paper now – it’s easier than chasing it later when the underwriter flags a missing item.

Bottom line? Those supplementary files are the quiet heroes that turn a good application into a great one. A well‑organised set of gift letters, rental evidence, insurance certificates, and legal paperwork shows the lender you’ve thought ahead, reducing the chance of “additional information required” emails and keeping your mortgage journey on track.

Now that you’ve got the full checklist, you’re ready to hit the portal with confidence. The lender will see a complete, transparent picture – and you’ll be one step closer to unlocking the front door of your new home.

Now that you’ve got the full checklist, you’re ready to hit the portal with confidence. The lender will see a complete, transparent picture – and you’ll be one step closer to unlocking the front door of your new home.

FAQ

What documents do I need for a mortgage if I’m a first‑time buyer?

First‑timers usually start with the basics: a valid passport or driving licence, a recent utility bill for proof of address, the last three payslips plus your P60 (or SA302 and tax returns if you’re self‑employed), and three months of bank statements for every account you hold. Add any existing debts – credit‑card statements, personal loan letters – so the lender can see the full picture. A quick tip is to name each file clearly, like “2024‑03‑Payslip‑March.pdf”, and store them in one folder ready for upload.

Do I need to provide proof of my deposit source?

Yes. Lenders want to know where your deposit came from to avoid money‑laundering concerns. If it’s savings, a recent bank statement showing the balance is enough. If a family member gifted you cash, you’ll need a signed gift letter and a copy of the donor’s bank statement confirming the transfer. This extra step can prevent “additional information required” emails later on.

How far back should my bank statements go?

Most UK lenders ask for the last three months of statements for every personal, savings, and joint account you own. If you have an overseas account, pull the equivalent three‑month extract in English if possible. Make sure the statements are dated within the last six months – anything older looks stale and may raise questions.

What if I’m self‑employed or have mixed income?

Self‑employed borrowers need a bit more paperwork: SA302 tax calculations for the past two tax years, full self‑assessment tax returns, and a profit‑and‑loss statement prepared by an accountant. If you also have a part‑time salary, include the three payslips and P60 for that side too, then add a short cover note that adds both income streams together. The goal is to give the underwriter one clean number to work with.

Are rental income and buy‑to‑let documents required?

If you own a rental property, lenders will ask for the tenancy agreement, the last six months of rent rolls, and any recent valuation report. Even if you only rent out a spare room on Airbnb, a summary of the platform’s payout statements helps boost your affordability calculation. Think of it as proof that the property is already generating cash, which can shave a few percent off your rate.

Do I need a valuation or survey before applying?

Not for the initial document checklist, but once the lender moves to valuation they’ll request a professional RICS‑registered survey. Having a recent valuation on hand (especially for an existing property you’re remortgaging) can speed up that stage. If you haven’t ordered one yet, a quick online request won’t hurt – it shows you’re proactive.

What extra paperwork can make my application stand out?

Beyond the mandatory list, a few optional items can give you a leg up: a one‑page debt summary that lists each credit‑card, loan, and monthly repayment; a “balance confirmation” letter from your bank for any high‑interest savings you plan to use as extra cash; and any insurance certificates for the new home. These extras signal organisation and low risk, making the underwriter’s job easier and often leading to a faster approval.

Conclusion

So, you’ve walked through every document the lender will ask for – ID, income proof, credit history, property papers and those extra bits that make your file shine.

If you’re still wondering whether you’ve missed anything, picture this: the underwriter opens your folder, sees neatly‑named PDFs like “2024‑03‑Payslip‑March.pdf”, a one‑page debt snapshot, and a short note explaining a recent bonus. In seconds they’ve got a clear story, and you’re one step closer to the keys.

What’s the next move? Grab a quick final checklist, tick each item, and upload everything to your lender’s portal before they ask. A tidy digital folder saves you from frantic last‑minute hunts and keeps the process moving smoothly.

And remember, you don’t have to go it alone. A Mortgage Mapper advisor can give you a quick once‑over, spot any hidden gaps, and even suggest that extra balance confirmation letter that could shave a few percent off your rate.

So, when the lender finally says “approved”, you’ll know you earned it by being organised, transparent, and a little bit proactive. Congrats – you’re about to turn that paperwork into a new front door.

Ready to get started? Open your file, give it a final glance, and hit submit. The smoother your document game, the faster you’ll hear the good news.

![What Is The Minimum Down Payment (Deposit) For A House In The Uk? [2026][Short Version]](https://mortgagemapper.com/featured-images/what-is-the-minimum-down-payment-deposit-for-a-house-in-the-uk-2026-short-version.jpg)